Introduction: Why These Sections Exist

Tax evasion has always been a major challenge for governments worldwide. India is no exception to this problem. Consequently, the Income Tax Act, 1961, contains several specific provisions to tackle hidden income.

Sections 68 to 69D are among the most powerful of these provisions. Together, they deal with unexplained cash credits, investments, expenditure, and transactions. Furthermore, they ensure that any unaccounted wealth is brought into the tax net.

These sections are not new. However, their importance has grown significantly over the years. Moreover, amendments over time have made them far stricter and more comprehensive.

The Core Philosophy Behind These Sections

Shifting the Burden of Proof

Normally, the Income Tax Department must prove that income exists. However, Sections 68 to 69D reverse this burden. Under these sections, the taxpayer must explain the nature and source of money or assets.

This reversal is deliberate and significant. It prevents taxpayers from simply denying the existence of income. Furthermore, it forces transparency in financial dealings.

Deeming Fiction

Each section creates what lawyers call a “deeming fiction.” In other words, certain amounts are deemed to be income even if the taxpayer claims otherwise. Consequently, such deemed income is fully taxable under the Act.

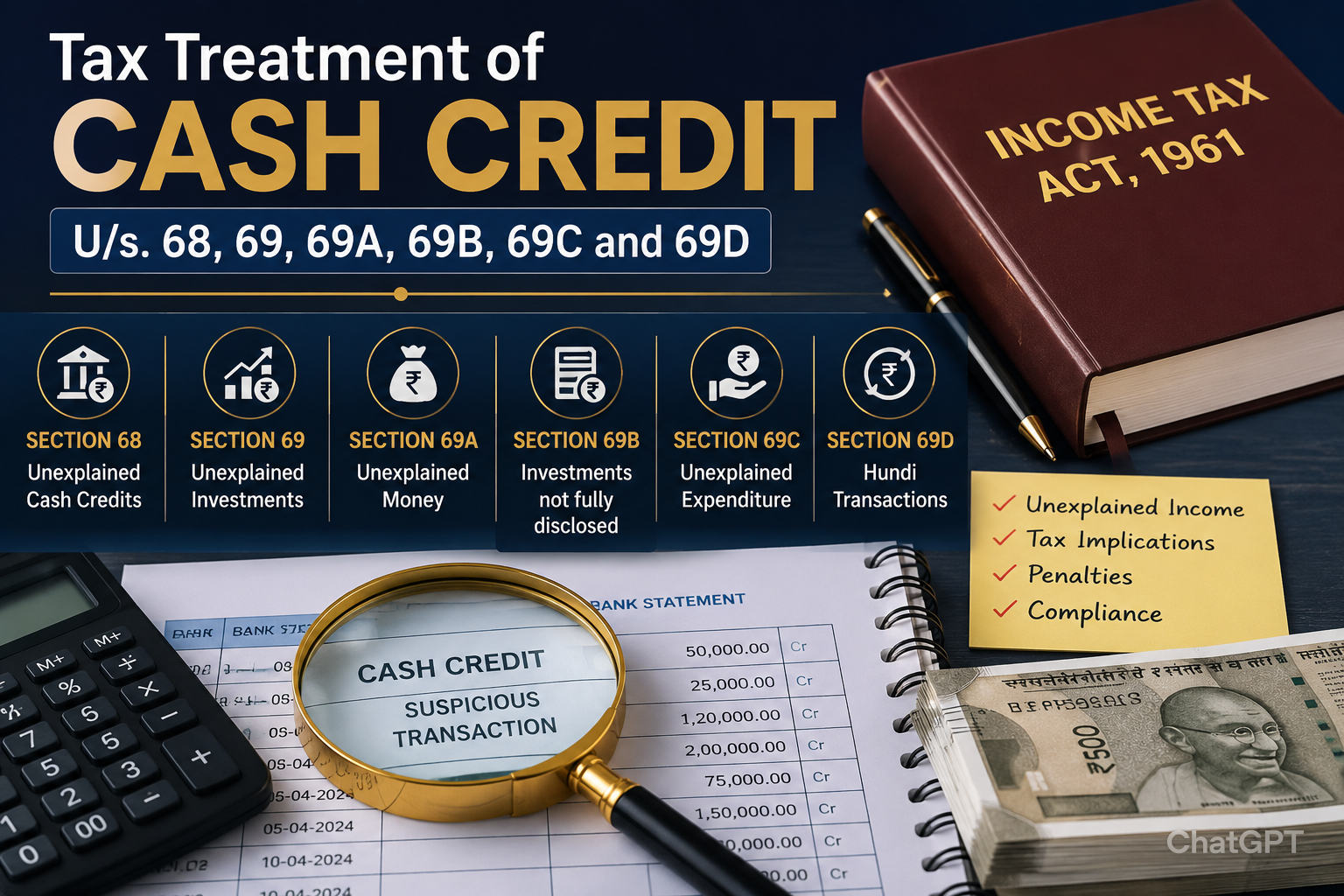

Section 68 — Cash Credits

The Statutory Provision

Section 68 reads as follows in substance: where any sum is found credited in the books of a taxpayer, and the taxpayer offers no satisfactory explanation about the nature and source of that sum, it may be charged to income tax as the income of that year.

What Are “Books of Account”?

Books of account include ledgers, journals, cash books, bank statements, and vouchers. Moreover, they include any document maintained for recording financial transactions. Consequently, any entry in any of these documents comes under Section 68’s scope.

The Three-Pronged Test

Courts have consistently laid down a three-part test under Section 68. First, the taxpayer must establish the identity of the creditor or depositor. Second, the taxpayer must prove the creditworthiness of that person. Third, the genuineness of the transaction must be established beyond doubt.

All three conditions must be satisfied simultaneously. Failure to satisfy even one condition invites an addition under Section 68.

Identity of the Creditor

Identity means more than just a name or address. The creditor must be a real, existing person or entity. Furthermore, the taxpayer must be able to produce supporting documents such as PAN card copies, confirmation letters, and bank statements of the creditor.

In many cases, taxpayers produce accommodation entry operators as creditors. However, courts have consistently rejected such entries. Consequently, identity must be genuine and verifiable.

Creditworthiness of the Creditor

Creditworthiness means the creditor must have the financial capacity to lend or invest the credited amount. For example, if a person with no income invests ₹1 crore as a shareholder, the AO can question creditworthiness.

The burden lies on the taxpayer to prove this. Moreover, the taxpayer must produce income tax returns, bank statements, and financial records of the creditor. Without such proof, creditworthiness remains unestablished.

Genuineness of the Transaction

Genuineness means the transaction must have actually taken place. Furthermore, it must have a legitimate business purpose. A mere bookkeeping entry does not establish genuineness.

Genuineness is typically proved through bank statements showing actual fund flows. Additionally, loan agreements, receipts, and correspondence help establish genuineness. Cash transactions, on the other hand, are always viewed with suspicion.

Share Capital and Share Premium

Section 68 has a specific explanation for closely held companies. In such companies, when shareholders invest money as share capital or share premium, the company must prove the source of funds. Moreover, the company must establish the identity and creditworthiness of all shareholders.

This explanation was inserted to curb the practice of routing black money through shell companies. Consequently, even a single unverified shareholder can lead to an addition under Section 68.

Key Judicial Rulings on Section 68

CIT v. Lovely Exports (P) Ltd. (2008): The Supreme Court held that if shareholders are assessed to tax and their identity is established, the company cannot be treated as having unexplained income. This was a landmark ruling protecting genuine companies.

Sumati Dayal v. CIT (1995): The Supreme Court held that human probabilities must guide the AO. If the explanation is humanly impossible, it can be rejected.

PCIT v. NRA Iron and Steel Pvt. Ltd. (2019): The Supreme Court held that mere identity is not enough. The AO must examine creditworthiness and genuineness too. This ruling reinforced the three-pronged test.

Section 69 — Unexplained Investments

The Statutory Provision

Section 69 applies when a taxpayer makes an investment in any financial year. However, the investment is not recorded in the books of account. Additionally, even if recorded, the taxpayer offers no satisfactory explanation of the nature and source of funds used for the investment.

In either case, the AO may treat the value of the investment as the income of that year.

What Constitutes an Investment?

Investments under Section 69 are broadly interpreted. They include purchase of land, buildings, shares, mutual funds, fixed deposits, and business assets. Furthermore, any application of funds for acquiring an asset qualifies as an investment.

The section does not restrict itself to financial investments alone. Therefore, even physical assets like machinery or vehicles come within its scope.

Off-Books Investments

The most common scenario under Section 69 involves off-books transactions. For example, a taxpayer may purchase property partly in white money and partly in black money. Consequently, the cash component often remains unrecorded.

When the AO discovers the unrecorded portion, it gets added as income under Section 69. Moreover, stamp duty valuations are often used to determine the actual investment value.

Valuation of Investment

A key question under Section 69 is: what value is added as income? The answer is the fair market value of the investment. Therefore, if a taxpayer bought land at ₹50 lakhs but shows only ₹30 lakhs, the AO adds ₹20 lakhs under Section 69B (discussed later).

However, if the investment is entirely off-books, the full market value is added under Section 69. Consequently, the taxpayer faces tax on an amount that may be several times the original investment cost.

Burden of Proof

Under Section 69, the burden of proof squarely rests on the taxpayer. Furthermore, the AO does not need to prove that the investment came from taxable income. It is sufficient for the AO to show that the investment exists and is unexplained.

Section 69A — Unexplained Money, Jewellery, and Valuables

The Statutory Provision

Section 69A covers money, bullion, jewellery, or other valuable articles. These must be found in the possession or control of the taxpayer. However, they must not be recorded in the books. Moreover, even if recorded, the explanation must be satisfactory.

If neither condition is met, the AO may treat the value of these items as income.

Scope of “Valuable Articles”

The phrase “valuable articles” is broad and covers many items. It includes gold, silver, diamonds, and other precious stones. Furthermore, it covers antiques, paintings, luxury watches, and other high-value movable assets.

Importantly, the section uses the word “possession or control.” Therefore, even items held by a third party on behalf of the taxpayer can be covered.

Relevance During Search Operations

Section 69A is most frequently applied during search and seizure operations. When tax authorities conduct raids, they often find unrecorded jewellery or cash. Consequently, Section 69A is immediately invoked to treat such finds as income.

The Central Board of Direct Taxes (CBDT) has issued circulars on this. For instance, there are specific guidelines on how much jewellery is considered normal for families. However, anything beyond those limits must be explained satisfactorily.

CBDT Instruction on Jewellery

As per CBDT Instruction No. 1916 of 1994, certain limits apply. A married woman may hold up to 500 grams of gold jewellery. Moreover, an unmarried woman may hold up to 250 grams. Additionally, a male member of the family may hold up to 100 grams.

Jewellery within these limits is generally not questioned. However, any excess beyond these limits must be explained by the taxpayer.

Key Judicial Rulings on Section 69A

Smt. Amiya Bala Paul v. CIT (2003): The Calcutta High Court held that the taxpayer must explain the source of unrecorded valuables. Inheritance claims without supporting evidence are not acceptable.

ITO v. K. Mahadev Naidu: The Tribunal held that long-standing family jewellery with proper pedigree need not be fully explained if the quantities are reasonable.

Section 69B — Amount of Investment Not Fully Disclosed

The Statutory Provision

Section 69B applies when a taxpayer has made an investment that is recorded in books. However, the amount shown in books is less than the actual cost of the investment. In that case, the AO may add the difference to the taxpayer’s income.

How Is This Different From Section 69?

Section 69 applies when the investment is entirely off-books. In contrast, Section 69B applies when the investment is partially disclosed. Therefore, Section 69B targets under-reporting rather than non-reporting.

Both sections, however, lead to the same result: the unexplained portion is treated as income.

Valuation Under Section 69B

Valuation is a critical issue under this section. The AO typically refers to stamp duty values, market valuations, or expert appraisals. Consequently, taxpayers often dispute the valuation methodology adopted by the AO.

Courts have held that the AO must use reasonable and fair methods of valuation. Furthermore, the taxpayer must be given an opportunity to contest the valuation. Arbitrary or excessive valuations have been struck down by courts.

Common Scenarios Under Section 69B

The most common scenario involves real estate transactions. A taxpayer buys property worth ₹1 crore but registers it for ₹60 lakhs to save stamp duty. The remaining ₹40 lakhs is paid in cash and remains unrecorded.

Consequently, the AO invokes Section 69B to add ₹40 lakhs as income. Moreover, Section 43CA and Section 56(2)(x) may also apply in such cases, creating further tax liability.

Interplay With Section 50C

Section 50C deals with capital gains on sale of land or buildings. It uses stamp duty value as the deemed consideration for computing capital gains. However, Section 69B deals with the buyer’s side of the transaction.

Therefore, both sections can apply to the same transaction from two different angles. As a result, real estate transactions involving under-reporting are heavily penalised.

Section 69C — Unexplained Expenditure

The Statutory Provision

Section 69C applies when a taxpayer incurs expenditure in any financial year. However, the source of such expenditure is not explained satisfactorily. In that event, the AO may treat the unexplained expenditure as income of that year.

The Unique Double Disadvantage

Section 69C is uniquely harsh compared to other provisions. Not only is the unexplained expenditure treated as income, but it is also not allowed as a deduction. Therefore, the taxpayer suffers in two ways simultaneously.

First, the expenditure is added as income and taxed at the flat rate of 60%. Second, the same amount cannot be deducted from business income. Consequently, the effective tax burden can exceed the actual expenditure itself.

What Qualifies as Unexplained Expenditure?

Expenditure qualifies under Section 69C if its source cannot be explained. Common examples include high-value cash payments for purchases, unexplained personal expenses, and payments to ghost suppliers. Furthermore, inflated expenses without proper documentation also attract this section.

The AO may estimate unexplained expenditure based on lifestyle analysis, property maintenance costs, or business pattern analysis. Consequently, even indirect evidence can trigger Section 69C.

Bogus Purchases and Section 69C

One major area where Section 69C applies is bogus purchase claims. Taxpayers sometimes claim purchases from non-existent suppliers to reduce taxable income. However, when these suppliers are found to be fictitious, the AO disallows the purchases.

Moreover, the amount is treated as unexplained expenditure under Section 69C. Therefore, it is added back to income and also denied as a deduction. Consequently, bogus purchases attract very heavy tax consequences.

Key Judicial Rulings on Section 69C

CIT v. Ratan Lal Sharma: The court held that where purchases are found to be bogus, the entire purchase amount can be treated as unexplained expenditure.

DCIT v. Shri Sanjay Baweja: The Tribunal observed that only the profit element should be disallowed in trading cases, not the entire purchase. This remains a contested area with varying judgments.

Section 69D — Amount Borrowed or Repaid Through Hundi

The Statutory Provision

Section 69D is one of the most unique provisions in the Act. It applies when any amount is borrowed through a hundi or repaid through a hundi. In either case, the amount is treated as income of the person who borrowed or repaid it.

What Is a Hundi?

A hundi is a traditional negotiable instrument originating in South Asia. It is used to transfer money or credit between parties, often without formal documentation. Moreover, hundis operate largely outside the banking system.

Historically, hundis were used by merchants and traders for inter-city fund transfers. However, they later became tools for routing unaccounted money. Consequently, Section 69D targets this practice directly.

The Unique Taxation Under Section 69D

Unlike most other provisions, Section 69D taxes both the borrowing and the repayment. Therefore, if a person borrows ₹10 lakhs through a hundi, it is treated as income. When the same person repays the ₹10 lakhs, that repayment is also treated as income.

As a result, the taxpayer is effectively taxed twice on the same amount. This harsh treatment is intentional and is designed to completely deter hundi transactions.

Practical Decline of Hundi Transactions

Thanks to Section 69D and other provisions, hundi transactions have significantly declined. Moreover, financial inclusion initiatives and digital payment systems have further reduced their usage. Consequently, Section 69D is less frequently invoked today compared to earlier decades.

However, in certain trading communities and rural areas, hundis still operate. Therefore, Section 69D remains a relevant and active provision.

Section 115BBE — The Special Tax Rate

Why a Special Rate Was Introduced

Before 2012, income under Sections 68 to 69D was taxed at normal slab rates. However, many taxpayers found ways to minimise tax even on unexplained income. Therefore, the government introduced Section 115BBE to impose a flat and harsh tax rate.

The Current Tax Rate

Under Section 115BBE, unexplained income under Sections 68 to 69D is taxed at 60%. Additionally, a surcharge of 25% is levied on this tax. Furthermore, a health and education cess of 4% is added on the tax and surcharge.

Therefore, the effective tax rate works out as follows:

- Base tax: 60%

- Surcharge: 25% of 60% = 15%

- Total before cess: 75%

- Cess: 4% of 75% = 3%

- Effective total tax: 78%

Consequently, if a taxpayer has unexplained income of ₹1 crore, the tax payable is approximately ₹78 lakhs. This leaves only ₹22 lakhs in the hands of the taxpayer.

No Deductions or Set-Off Allowed

Section 115BBE is extremely strict about deductions. No expenditure can be claimed against income covered under Sections 68 to 69D. Moreover, no loss from any other source can be set off against this income.

Additionally, carry-forward losses cannot be adjusted either. Therefore, the full unexplained amount is taxed without any relief whatsoever. Consequently, this is one of the highest effective tax rates in Indian income tax law.

Amendment After Demonetisation

Section 115BBE was significantly amended after demonetisation in November 2016. Before the amendment, the tax rate was 30%. However, the Finance Act, 2016 increased it to 60% to discourage post-demonetisation black money disclosures.

Furthermore, an additional 10% penalty was introduced for unexplained income detected during search operations. Consequently, the post-demonetisation changes made the provision far more punitive.

Penalties in Addition to Tax

Section 271AAB — Penalty During Search

When unexplained income under Sections 68 to 69D is found during a search, Section 271AAB applies. This section imposes a penalty of 30% if the income is admitted during search and surrendered. However, if income is not admitted, the penalty rises to 60% of the tax.

Consequently, a taxpayer who admits during search pays 30% penalty on 60% tax. In total, this amounts to approximately 96% of unexplained income being taken away by the government.

Section 270A — Penalty for Under-Reporting

Apart from Section 271AAB, Section 270A imposes penalties for under-reporting or misreporting of income. Under-reporting attracts a penalty of 50% of the tax. Misreporting, which is more serious, attracts a penalty of 200% of the tax.

Therefore, taxpayers who conceal income under Sections 68 to 69D face both tax under Section 115BBE and penalties under Section 270A or 271AAB.

Prosecution Risk

Beyond penalties, repeated tax evasion can lead to prosecution under Section 276C. This section allows imprisonment of up to seven years for wilful tax evasion. Furthermore, conviction can result in both imprisonment and fines.

Consequently, the combination of high tax rates, penalties, and prosecution risk makes concealment extremely costly.

The Assessment Process Under These Sections

How the AO Discovers Unexplained Income

The AO discovers unexplained income through multiple channels. These include scrutiny assessments, survey operations, search and seizure, third-party information, and annual information returns. Furthermore, the Annual Information Statement (AIS) now captures most financial transactions automatically.

As a result, the tax department has access to more data than ever before. Consequently, hiding income has become far more difficult in the digital age.

Show Cause Notice and Opportunity to Explain

Before making any addition under Sections 68 to 69D, the AO must issue a show cause notice. Furthermore, the taxpayer must be given a fair opportunity to respond. This is a fundamental principle of natural justice.

The taxpayer can respond with documents, affidavits, and explanations. If the AO is satisfied, no addition is made. However, if the explanation is rejected, the AO passes an assessment order adding the unexplained amount to income.

Appeal Rights of the Taxpayer

Every taxpayer has the right to appeal against additions under these sections. First, the taxpayer can appeal before the Commissioner of Income Tax (Appeals). Thereafter, the taxpayer can approach the Income Tax Appellate Tribunal (ITAT).

Further appeals lie before the High Court and the Supreme Court on questions of law. Consequently, taxpayers with genuine cases can seek justice at multiple levels.

Practical Guidance for Taxpayers

Maintain a Trail for Every Large Transaction

Every large receipt, investment, or expenditure must have a complete paper trail. Bank statements showing actual fund flows are the most powerful evidence. Moreover, documents must be contemporaneous, meaning they must exist at the time of the transaction.

Creating documents after the fact is treated as fabrication. Consequently, courts and AOs reject retrospectively created documents.

Use Banking Channels for All Significant Transactions

The income tax law strongly encourages the use of banking channels. Under Section 269SS, loans above ₹20,000 cannot be accepted in cash. Moreover, Section 269T prohibits repayment of loans above ₹20,000 in cash.

Violations of these sections attract penalties equal to the amount of the transaction. Therefore, using banking channels protects taxpayers both from these penalty provisions and from scrutiny under Sections 68 to 69D.

Declare All Income Honestly Every Year

The simplest and most effective way to avoid trouble is honest disclosure. Declaring all income, including income from all sources, in the annual return protects the taxpayer. Moreover, it creates a consistent financial history that stands up to scrutiny.

Furthermore, the Voluntary Compliance Encouragement Scheme and similar past schemes showed that honest disclosure is always better than concealment.

Respond to Notices Promptly and Thoroughly

Many assessments under these sections result from inadequate responses to notices. Therefore, every notice from the tax department must be taken seriously. Furthermore, the taxpayer should engage a qualified tax professional immediately upon receipt of any notice.

A prompt and well-documented response can prevent unnecessary additions to income. Consequently, timely and thorough communication with the tax department is always beneficial.

Interplay With Other Provisions

Section 68 and Section 56(2)

Section 56(2) deals with income from other sources, including gifts and receipt of shares at less than fair market value. Consequently, there is sometimes an overlap between Section 68 and Section 56(2).

For example, if a company receives share premium from shareholders, both sections could potentially apply. However, the courts have generally held that Section 68 is the more specific provision and takes precedence in such cases.

Section 69 and Section 50C

Section 50C deems stamp duty value as sale consideration for computing capital gains on immovable property. In contrast, Section 69 deals with unexplained investments by the buyer.

Therefore, when a property transaction involves under-reporting, the seller faces scrutiny under Section 50C while the buyer faces scrutiny under Section 69 or 69B. As a result, both parties to the same transaction can face additions to income.

Section 69C and Section 37

Section 37 allows deduction of business expenditure. However, expenditure must be legitimate, documented, and incurred for business purposes. If the AO finds expenditure to be unexplained, Section 69C overrides Section 37.

Consequently, the expenditure is not only disallowed but also treated as income. Therefore, bogus or inflated expenses result in a far worse outcome than legitimate expenses.

Recent Developments and Trends

Project Insight and Data Analytics

The Income Tax Department launched Project Insight to leverage data analytics. This system matches data from multiple sources to identify discrepancies in tax returns. Furthermore, it flags taxpayers whose lifestyle and investments do not match declared income.

As a result, Sections 68 to 69D are being invoked more frequently based on data-driven analysis. Consequently, the era of hiding income through informal channels is rapidly ending.

Faceless Assessment

Under the Faceless Assessment Scheme introduced in 2019, assessments happen online without personal interaction. Consequently, the process has become more objective and transparent. Moreover, additions under Sections 68 to 69D are now reviewed by multiple officers before being confirmed.

This has, to some extent, reduced arbitrary additions. However, it has also made the process faster and more efficient for the tax department.

Annual Information Statement (AIS)

The AIS now captures nearly every significant financial transaction of a taxpayer. This includes property registrations, high-value bank deposits, mutual fund investments, and credit card expenses. Furthermore, all this data is pre-filled in the taxpayer’s AIS portal.

Consequently, any discrepancy between AIS data and the tax return automatically triggers scrutiny. Therefore, unexplained differences are now detected with far greater speed and accuracy.

Summary of All Six Sections

| Section | Trigger | What Is Added | Special Feature |

|---|---|---|---|

| 68 | Unexplained cash credit in books | The entire credited sum | Covers loans, share capital, gifts |

| 69 | Unrecorded investment | Fair market value of investment | Covers all types of assets |

| 69A | Unrecorded money, jewellery, valuables | Value of the items found | Applies strongly during search |

| 69B | Understated investment value in books | The understated/difference amount | Targets under-reporting specifically |

| 69C | Unexplained expenditure | The unexplained expenditure amount | No deduction allowed; double impact |

| 69D | Hundi borrowing or repayment | The borrowed or repaid amount | Both borrowing and repayment taxed |

All the above are taxed at 60% flat under Section 115BBE, plus 25% surcharge and 4% cess, making the effective rate approximately 78%.

Conclusion

Sections 68 to 69D are not merely technical provisions. Together, they form a comprehensive framework to combat black money and tax evasion. Moreover, when combined with Section 115BBE and the penalty provisions, they make concealment of income an extremely costly affair.

The message from the legislature is clear. Honest and transparent financial dealings are not just morally right; they are also economically the most sensible choice. Furthermore, with data analytics, AIS, and faceless assessments, the chances of detection have never been higher.

Therefore, every taxpayer, whether an individual, firm, or company, must maintain clean and well-documented books of account. Additionally, all large transactions must flow through banking channels with proper documentation. Ultimately, compliance today is far cheaper than concealment discovered tomorrow.

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

Recent Comments