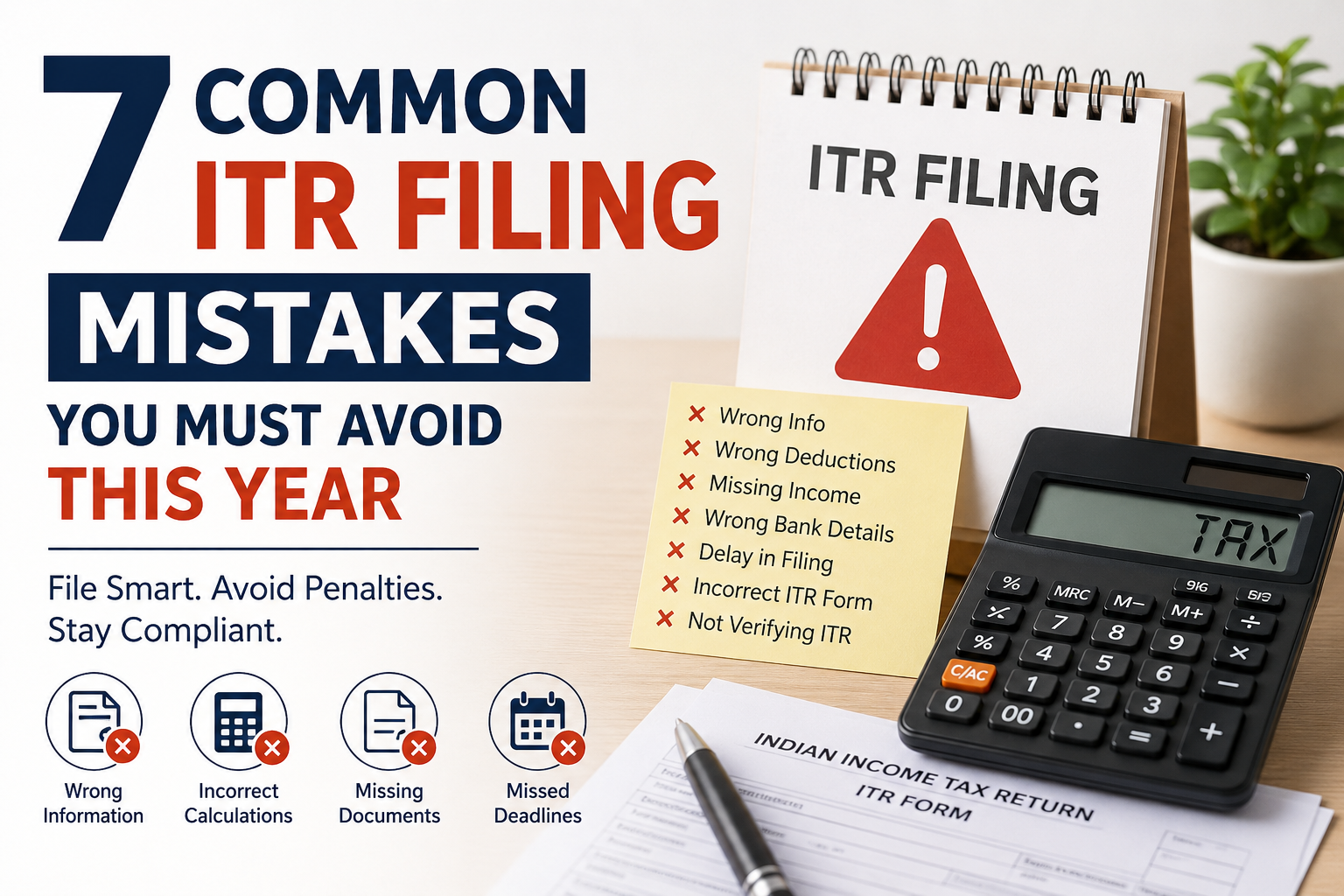

Filing your Income Tax Return (ITR) is a crucial annual responsibility. However, even small errors can trigger tax notices, delays, or extra demands. Therefore, understanding these common mistakes helps you file correctly the first time.

Why Getting Your ITR Right Matters

Every year, millions of taxpayers rush through their ITR filing. As a result, many end up making avoidable errors. Consequently, the Income Tax Department sends notices that cause unnecessary stress. So, let us walk through the seven most common mistakes — and how to avoid them.

Mistake 1: Claiming Deductions Without Proper Proof

Many taxpayers claim deductions under Section 80C, 80D, or other sections carelessly. However, they forget to keep supporting documents ready. For instance, a life insurance receipt or a PPF passbook is essential proof.

Additionally, the tax department may ask you to justify every deduction you claim. Therefore, always collect and save your investment proofs before filing. Moreover, digital copies stored in a folder make the process much easier.

Mistake 2: Not Reconciling AIS, Form 26AS, and TDS Details

Your Annual Information Statement (AIS) and Form 26AS reflect all financial transactions linked to your PAN. Furthermore, they show TDS deducted by your employer or bank. Ignoring these documents is a serious mistake.

Consequently, if your ITR figures do not match these records, the system flags a mismatch. As a result, you may receive a demand notice from the Income Tax Department. Therefore, always cross-check these documents before you submit your return.

Mistake 3: Choosing the Wrong ITR Form

India has multiple ITR forms — ITR-1, ITR-2, ITR-3, ITR-4, and more. Each form suits a specific category of taxpayer. For example, ITR-1 is only for salaried individuals with basic income sources.

However, many taxpayers pick the wrong form out of confusion. Unfortunately, filing with the wrong form makes your return defective. Therefore, always check the eligibility criteria for each form carefully before proceeding.

Mistake 4: Not Reporting All Income Sources

Many people only report their salary or business income on their return. Nevertheless, the law requires you to report every source of income. For example, savings account interest, fixed deposit interest, and rental income must all be declared.

Furthermore, if you hold foreign assets or earn income abroad, you must report that too. Failing to do so attracts serious penalties under the Black Money Act. Therefore, think carefully about every income stream before submitting your return.

Mistake 5: Incorrect or Incomplete Capital Gains Reporting

Selling mutual funds, shares, or property generates capital gains. Moreover, these gains attract tax depending on the holding period. Short-term and long-term gains follow different tax rules entirely.

However, many taxpayers either skip reporting these gains or calculate them incorrectly. As a result, the tax department can raise a demand with interest and penalties. Therefore, use accurate purchase and sale records to compute your capital gains correctly.

Mistake 6: Missing the Due Date for Filing

The standard ITR filing deadline for salaried individuals is July 31 each year. However, many people procrastinate and miss this date entirely. Subsequently, late filing attracts a penalty of up to ₹5,000 under Section 234F.

Additionally, missing the deadline means you lose the chance to carry forward most losses. Therefore, mark the due date on your calendar well in advance. Moreover, filing early gives you time to correct errors without pressure.

Mistake 7: Failing to Verify the Return After Submission

Submitting your ITR is not the final step — verification is. Surprisingly, many taxpayers forget to e-verify their return after filing. As a result, their return is treated as invalid, even though they submitted it on time.

Fortunately, you can verify your return easily through Aadhaar OTP, net banking, or a signed ITR-V sent by post. Furthermore, the verification must be completed within 30 days of submission. Therefore, always confirm your return is verified before you consider the process complete.

Quick Summary: 7 Mistakes to Avoid

| # | Mistake | Risk |

|---|---|---|

| 1 | No proof for deductions | Disallowed claims |

| 2 | Skipping AIS/26AS check | Mismatch notice |

| 3 | Wrong ITR form | Defective return |

| 4 | Unreported income | Penalty + interest |

| 5 | Wrong capital gains | Tax demand |

| 6 | Late filing | ₹5,000 penalty |

| 7 | No verification | Invalid return |

Final Thoughts

ITR filing does not have to be stressful. In fact, a little preparation goes a long way toward a smooth, error-free submission. Additionally, consulting a tax professional for complex cases is always a smart choice. Above all, accuracy and timeliness protect you from unnecessary tax trouble.

So, take your time, gather your documents, and file your ITR with confidence this year.

Recent Comments